Fixing Social Security

Part 1: What is Social Security For?

Post 58: 7 April 2026

There are two Social Security crises. The first is about funding: The trustees of the program report that the trust fund will most likely be depleted sometime during 2033. Without changes in the law, the program will have to reduce benefits (by 22%) to remain solvent.1 That’s a serious problem, more serious than earlier Social Security funding crises, but it is a solvable one. The second crisis is political, and it is more serious. Americans have little faith that Congress can fix the program’s technical issues.

Large majorities of Americans now believe that Social Security will not be there for them in retirement even though a substantial minority know they will have to rely on it as their primary source of income.2 That’s not a great mix. People are probably right about how much they personally need the program. Surveys of current seniors show that Social Security is the only source of income for more than one-quarter and makes up more than half of the income of two-thirds.3 The result is that a growing number of working-age Americans are losing faith in the idea of retirement. A recent TIAA survey found that 30% of Americans felt that they would not be able to retire at “retirement age” but instead work until physically unable to.4

Though sincere, the personal pessimism about individual retirement options is often exaggerated—I need to say more about that at another time—but the political pessimism is well earned. Congress is as dysfunctional as at any moment in my lifetime. And political negotiations about Social Security are complicated by the fact that neoliberals (mostly in the Republican party) often conceal their deep preferences for privatizing or otherwise crippling the program.5 This lack of good faith inevitably leads to misdirection and misinformation and, yes, pessimism. The only way we can work through the political crisis is to address the practical problems. We need to set out our goals and values and use them to evaluate the technical options and tradeoffs. Once we expose the hidden agendas, the funding problem is not so daunting.

My plan is to approach this topic in several bites. Today, I will set out some basic principles that provide some desiderata for reform. Next week, I plan to review the structural and fiscal issues and outline some of the proposed fixes. I may spend a week describing some of the serious good faith efforts to repair the program. At some point, I’ll rant about some of the not-so-good-faith neoliberal efforts to undermine it. To keep things as simple as possible, I will mostly focus on retirement, that is on the approximately 52 million retirees receiving Social Security right now. I will leave survivors and those on disability for another time.6

Social Security and Social Citizenship

One of the tenets of social citizenship is that we all should have a set of life choices that are similar to others in our community. For those of us without physical impairments that force the issue, one of these choices will be when to stop working for pay. The idea suggested in the TIAA poll cited earlier that some of us will not, or already do not, have this choice is unacceptable, a violation of basic autonomy. Not every society has had the expectation of a healthy retirement, but in our society, it is a life choice we expect, and that means that everyone must be afforded this choice.

The traditional liberal, we would now say “neoliberal”, response to this assertion is that everyone has the right to retire but also the responsibility to prepare for retirement. Neoliberals would not recognize that the mere existence of this right confers a duty on the rest of us to ensure that everyone has the necessary resources. You made your bed.

The understanding of personal responsibility embedded in this view often conceals deep prejudices, is wildly unrealistic about how much any of us can prepare for what life throws at us and, by extension, how much we can depend on the “rugged individualism” they value so highly, is generally too optimistic about financial returns, and, perhaps most importantly, mistakes luck, mostly the luck of birth, as merit. The simple fact is that people often cannot prepare for all the exigencies of old age. Physical infirmity may shift timelines or raise costs, sometimes beyond the point for which anyone could prepare. Morally pressing demands on income may arise. Patterns of economic exploitation, or simple lack of opportunity, may place an absolute limit on our ability to save. And stuff can happen to flatten even the best-laid plans of whole generations: natural disaster, sickness, injury, war, and economic crisis. In the Depression years before the passage of Social Security, a majority of senior citizens lived in poverty.7 Were they all “irresponsible”?

Given all these uncertainties, we can, and did, decide to insure one another against the risk of running out of money in retirement. That was, and remains, the rational thing to do. That’s why, stripped of its ideological baggage, the vast majority of Americans approve of the approach. It is why Social Security is the most popular program of the federal government, and why most people think we should preserve, and even extend, the program, regardless of the nation’s fiscal situation.8

Setting the Level of Security

How generous should Social Security be? There is a constituency for simply accepting some or all of the projected 22% benefit cuts, especially among those who are angry that America does a much better job of taking care of seniors—who get Medicare and have a poverty rate of about 10%—than children—who have no universal health program and whose poverty rate is more like 15%.9 I too would like to see much greater investments in children, but this is not a zero-sum game. I will focus on evaluating the needs of retirees independently and still advocate for the next person.

Social citizenship requires that every person is able to participate fully in the community. It is always difficult to evaluate “adequacy” by this standard, but the concept is simpler among those for whom work is not, and is not expected to be, a primary part of what “participation” means. These folks aren’t preparing for or making big start-of-adult-life choices, so we can focus on whether they have enough resources to live a life that the rest of us would find acceptable. As our guide TH Marshall put it: “to live the life of a civilized being according to the standards prevailing in the society.”10 This means, I think, being able to live as independently as health allows and to meet basic needs without depending on charity. That requires a certain level of income, our focus today, but it also means that we have to set some guardrails around key costs, especially for healthcare and housing. This complication means that we cannot evaluate the income part of these requirements independently.

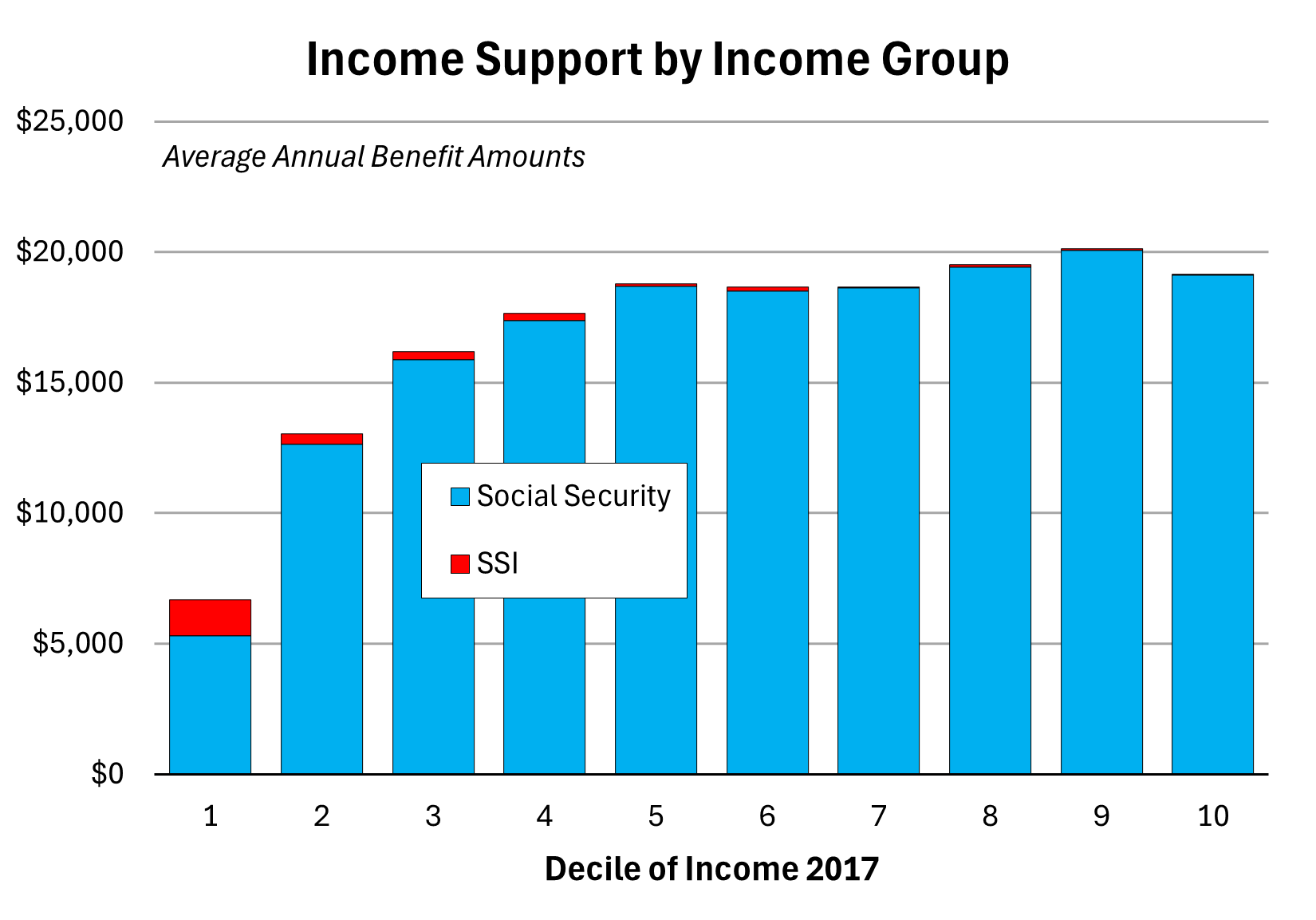

Arguably, the “typical” Social Security payment—about $1,900 per month in 2024— is reasonable if not completely adequate (since the average one-bedroom apartment rents for about $1500). By definition, though, half receive less than this median amount, with about 20% receiving $1,200 or less, which is close to the poverty threshold.11 We need to worry more about those who receive these lower benefit amounts, especially since these are exactly the people who are unlikely to have other sources of income. For a large swath of middle- to higher-income American seniors average Social Security payments are quite similar, but these payments are very low for the poorest decile of older households. Supplemental Security Income offsets this gap, but not nearly by or often enough. (See chart.)12 The eventual plateau in average annual benefits owes a great deal to the somewhat “progressive” structure of Social Security benefit calculations,13 but this does not help those with very low lifetime earnings. In the long run, raising federal minimum wages would do a great deal to repair this source of inequality, but a strong argument can be made for adjusting the “kink” points in the benefits calculation (more on that is possible next week) and/or simply augmenting benefits at the low end, either through Social Security or SSI, so that no senior citizen lives in poverty. This is a very attainable goal; I’ll try to price that out in the next week or so.

Part of the benefit inadequacy problem can be attributed to the loss of benefits that retirees (essentially) inflict upon themselves by choosing to collect benefits early. In 2024, the median initial benefit received by those retiring early (before their official “full retirement age” or FRA) was about $750 less than those retiring at FRA or later ($1550 vs $2300).14 Some reform of early retirement may also be in order, for several reasons. Most seriously, there is a class of workers who may now be choosing early retirement only because their jobs are too physically demanding. This may be a good option for them, but it may also put them at grave financial risk. We ought to have a way for these workers, without the extended and difficult process of establishing “disability”, to retire early without penalty, or a new program that can build a “bridge” to FRA for them.

There is also some evidence that some people take early retirement in response to poor labor market conditions. This also may be a valid option for them, but the choice to take this path begs the question: what other options ought to have been open?

In general, the timing of retirement ought to be actuarially neutral—whether one gets less for longer or gets more for less time is mostly a wash—but that is only true if the income stream that results is adequate. People ought to have this choice, but a forced choice is not a choice at all. The system ought to be structured so that we are free to choose what is best for ourselves. I again refer to the central tenets of social citizenship: we should all have comparable choices.

Goals for Reform

The principal goal of the next round of Social Security amendments has to be fiscal—that will be the focus of the next post—but the above discussion suggests that the program ought to be strengthened in a number of other ways. Since major Social Security legislation is rare, we should not waste the opportunity. So far, I have suggested that benefit levels are too low for retirees with the lowest incomes and that the retirement age is too high for workers with physically demanding jobs. Reforms in both of these areas will make the fiscal problem worse, and both suggestions go directly against some of the reforms people propose, such as cutting benefits or raising the age of full or early retirement. I believe a balanced approach can address both equity and solvency concerns, but have to leave it here for today.

<All of the posts in On Social Citizenship connect. I recommend that readers go back and read the first entry in the series.>

Next week (14 April 2026) I plan to continue the discussion of Social Security by reviewing the fiscal situation, possibly listing some of the many proposals for restoring actuarial balance (there are many).

OASDI Trustees, 2025 Annual Report. I’ll refer to this in the text as “Trustees”.

Bipartisan Policy Center, “New Poll: On 90th Anniversary of Social Security, Americans See It as Most Valuable Federal Program”. Here’s one quote: “74% of the public is concerned that Social Security will run out before they retire, and 80% are worried that Congress will cut benefits. Even so, 41% of Americans expect Social Security to be their primary source of income during retirement.” The TIAA survey (see note 4) similarly found that 44% believed that Social Security would have to be their “primary” source of income.

Alex Moore, “Two-Thirds of Seniors Rely on Social Security for More Than Half Their Income”, The Senior Citizens League.

TIAA, “Nearly Two-Thirds of Americans Feel Retiring ‘On-Time’ is Unattainable, According to New TIAA Survey”, October 6, 2025.

For example, in 2005, George Bush proposed that some Social Security payroll tax revenue be diverted to private accounts. Widely seen as the camel’s nose of complete privatization, the proposal never got as far as a Congressional vote.

There were 68.5 million OASDI beneficiaries in December 2024. These 51.8 million retirees, 2.5 million spouses, 5.8 million survivors, and 8.3 million disabled. (Trustees, 2025 Annual Report)

According to the Social Security Administration.

In 2025, the Bipartisan Policy Center found that 93% of Americans considered Social Security to be a “valuable” program, the most of any tested, and 83% believe that the program should be a budget “priority” regardless of the nation’s fiscal situation.

See Census Bureau, Poverty in the U.S., Current Population Survey, Table A-3.

T.H. Marshall, “Citizenship and Social Class,” in Marshall and Tom Bottomore, Citizenship and Social Class (Pluto, 1992), 8.

Only 10% of seniors live in poverty mostly because a majority live with spouses who also receive a check.

Daniel Thompson and Michael D. King, “Income Sources of Older Households: 2017” (Census Bureau, Current Population Reports, P70BR-177) February 2022. The lowest income seniors are by far the most likely to receive SSI payments, but only about one-quarter qualify for this support, which can be very hard to get, and SSI payments average less than $600 per month (Trustees).

This is complex. Briefly: benefits initially rise rapidly (90% of earnings) with wages for earnings below a quarter of the average wage (roughly), then at 32% until earnings are about 40% above average (again, roughly), but for earnings higher than this, the marginal benefit increase is only 15% or earnings. There is a maximum benefit because there is a maximum tax liability.

Trustees, Table 6.b3.