Paying for Retirement

Fixing Social Security, Part 3

Post 60: 21 April 2026

Last week, I made the general point that the “crisis” in Social Security was mostly attributable to slower than needed growth in wages, and therefore revenues. Since then, I ran into a report from the American Academy of Actuaries that concluded that

The population forecasts made in 1983 have generally stood the test of time, while economic factors fell short…. For the most part, the shortfall results from the growth of taxable payroll falling below expectations.1

I don’t want to lose sight of this basic insight as we debate policies to restore stability to the Trust Fund. Our best long-term response will be to increase wages. In the short-run, we still have a fiscal imbalance to fix using the policy levers to which it is directly attached—the payroll tax and the way that benefits are calculated and taxed—but as we make projections based on these policies, we should be working to undermine them, but this time in a good way by outperforming expectations. A wealthier working population can support more retirees.

Today, I want to talk a bit about the sorts of fixes available to us on the revenue side. We can generate enough income to keep the Trust Fund solvent without increasing the burden on the average person.

The Payroll Tax

Presently, 90% of the revenue for the Social Security program is drawn from a payroll tax of 12.4% on the first $184,500 of wages. This rate is split evenly, 6.2% paid directly by workers and 6.2% paid by employers, but there is little doubt that in equilibrium workers bear the whole burden of this tax, half directly and half through lower wages.2

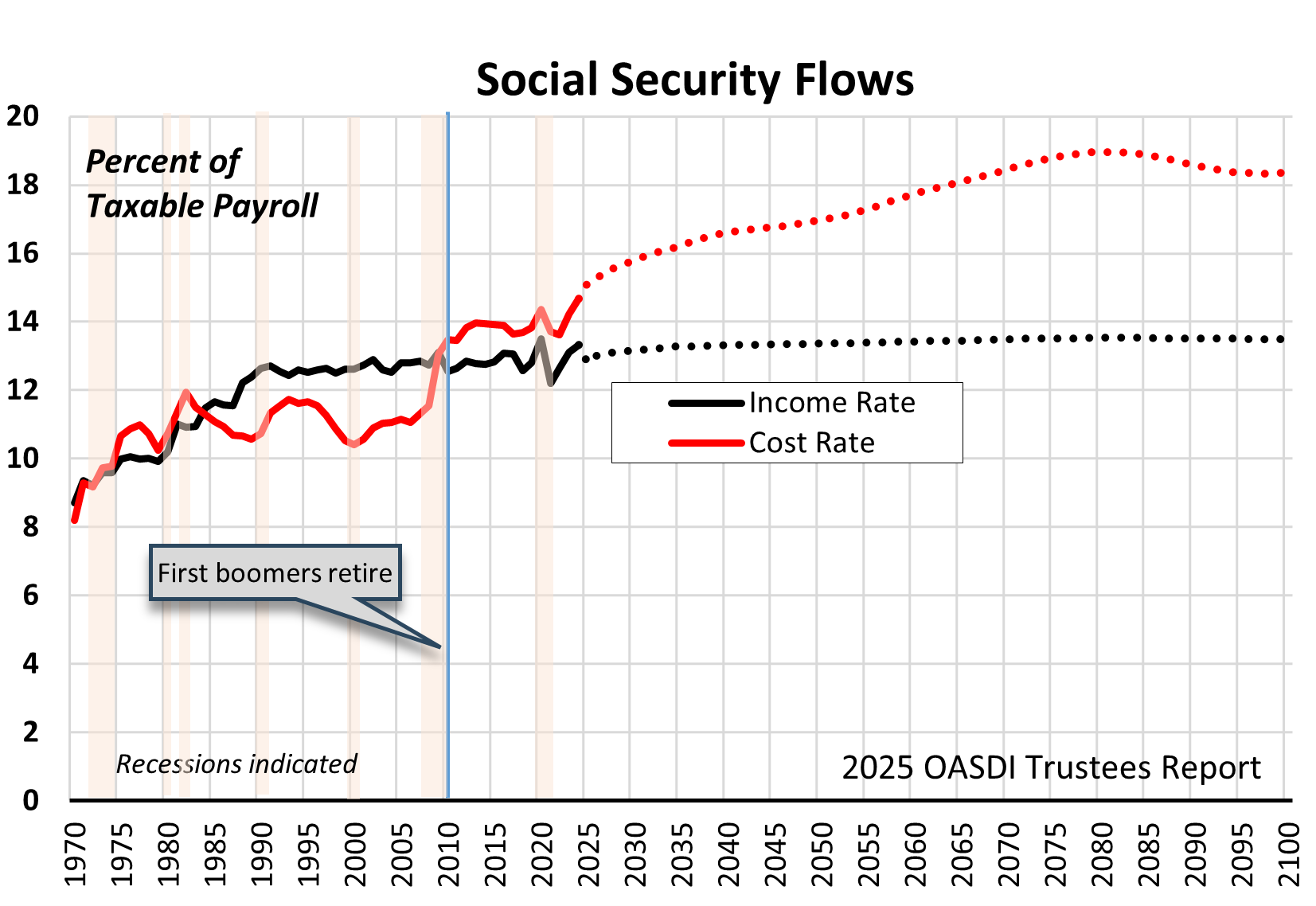

The chart at top depicts the flows in and out of the Trust Fund as percentages of taxable payroll. The “income rate” is our focus today. You can see that this rate has been fairly constant since the increases enacted in 1983 took full effect. The chart shows that the system produced an annual surplus for the whole period between 1984 and 2009 and an operating deficit since.

It is possible to restore balance simply by raising the payroll tax rate. Eyeballing the chart will give you a rough sense of the rates required on a year-to-year basis: we would have to raise the total payroll tax to something like 14% immediately, to 16% in the next decade, and finally to 18%. The middle position, which the Social Security Administration (SSA) has produced estimates for, would be to raise the payroll tax to 16.4% immediately (in 2026) and permanently. They project that this alone would keep the Trust Fund solvent for the rest of the century.3

That’s a helpful place to start. If this was all we did, we would have to increase the average tax rate on income by about 4 percentage points to keep this ship afloat. But that’s a lot, and we should not do this unless we absolutely have to. To put these rates in the context of the whole system of personal taxation: In 2025, Americans paid about 30% of their total compensation in personal taxes. On this base, a 4 point increase looms pretty large.4

Expanding the Base

We can and should fix the problem without raising the payroll tax at all.

The other major lever in the payroll tax system is the hard cap on taxable wages (now $184,500). That high a salary is reached by only 6.3% of salaried workers, but something like 17% of all wages are untaxed because of it. Simple math therefore says that we can raise the total income available to the fund by 20% (1/.83) simply by taxing all wages. This is equivalent to raising the payroll tax by about 2.5 points without raising taxes on anyone earning less than $184,500. That change alone would not solve the system’s fiscal problem—the exercise above suggested that an overall revenue increase of about one-third is needed—but the SSA estimates that this shift, by itself, would extend the life of the program by 20 years, to 2054.

I note that eliminating the tax cap also eliminates the benefit cap, so this proposal makes the cost problem worse over time. Some proposals would not increase benefits above this (or some higher)5 wage limit. While that change buys more time (about 5 years), it adds an unnecessary layer of complication to the system and introduces a new point of contention about fairness. A better approach is to count these benefits as income and increase the progressivity of the income tax. I’ll return to that theme in a moment.

Because wages and salaries represent only one-half of personal income, another way to increase the revenue base for Social Security is to expand the “payroll” tax to include other income streams. A group of Progressive Democrats, led by Bernie Sanders, have proposed included in the taxable base investment income and S-corp incomes, for example. Including investment income is equivalent to raising the payroll tax by about 1.25 points; adding S-corps income is equivalent to adding about 1 point to the payroll tax.6 Each of these changes, standing alone, would add about five years of solvency.

We have already outlined a workable proposal that could fund Social Security for the foreseeable future without raising payroll taxes. Taxing all wages, including pass-through income from S-corps in the wage bill, and taxing some investment income would, taken together, raise more revenue than raising the payroll tax by 4 points, enough, in fact, to increase benefits as well. This is why the Progressive reform proposals generally do not include any increase in the payroll tax rate, and neither would I.

Payroll Taxes and Income Taxes

Payroll taxes are just one form of income taxes, albeit a very clumsy and regressive one. How should it interact with the basic IRS-based tax?

In 2024, 4.4% of total income into the Trust Fund came from the taxation of Social Security benefits. This share will rise gradually because the relevant tax law does not include automatic inflation adjustments.7 The formula calculating it is complicated,8 but the tax affects about half of all retirees and mostly falls on those whose cash incomes (AGI plus benefits) are greater than $100,000 (see this CBPP analysis). In aggregate, the average tax rate on benefits is very low: the tax yield is only 4.1% of benefits paid.

Right now, the taxation of benefits is equivalent to about 0.5 points on the payroll tax. In theory, taxing Social Security as ordinary income makes more sense. This is how we tax private pension incomes. Under the current tax code, this would raise some revenue. The SSA estimates that this would be equivalent to an additional 0.25 points [about 50% more than presently but still only about 6% of all Trust Fund in-flows]. We should not make this change to improve the Trust Fund balance (though I think a fair system of taxation would do that), but to simplify and gain control over the tax code. Lower-income people ought to pay taxes at lower rates, but the easiest way to construct a fair tax schedule is to combine all forms of income on as close to a dollar-for-dollar basis as we can and apply a progressive exemption, deduction, and rate structure to this simple aggregate. A full examination of this topic will have to wait for another time, but we should not be taxing income differentially based on its source, rather than its value, unless we can make a compelling case for preferring one kind of income over another. People 100% reliant on Social Security should not pay an income tax, not because the source is Social Security, but because their incomes are too low to justify paying any tax. Indeed, they probably ought to pay a negative income tax, effectively raising their benefits that way. I’ll say a bit more about that when I discuss the benefit structure, which I plan to do next week.

There is a deeper issue here. Almost all “social security” (old age and disability pension) systems around the world depend almost solely on payroll taxes for funding. While this has the advantage of creating a secure and dedicated source of revenue for these programs, it ties eventual retirement benefits excessively to the labor market value of claimants. As I have noted, this still leaves too many American retirees in poverty. The flat payroll tax also skews the overall tax system in a regressive direction. We should be analyzing the adequacy and fairness of whole tax system instead of looking at each tax separately. There are reasons to tax wealth (real estate), consumption and other economic transactions, and incomes separately. These events capture different aspects of economic life and individual ability to pay. But if we are honest, we would admit that governments tax events that they can tax, that is, for which they have an administrative tax apparatus, rather than based on a coherent broader theory of taxation. The absence of an overarching framework is most apparent when we tax the same thing twice, which we do for wages. Broadening the base for the payroll tax to include non-wage incomes is the best solution for Social Security’s fiscal problems precisely because it would begin the process of placing this social burden on incomes rather than just wages. A better long-term solution would be to fund more, if not all, of the Social Security program through the income tax itself. But that is part of the larger conversation about how we ought to pay for the social rights of citizenship, a theme I hope to return to in the future.

Next week, I hope to turn to the cost side of Social Security. My focus, however, will not be to argue for cutting costs but for increasing them by strengthening the program.

<All of the posts in On Social Citizenship connect. I recommend that readers go back and read the first entry in the series.>

Notes

To this, we can also add that interest rates, especially after 2008, were much lower than the 1983 Amendment writers assumed, so the returns on the Trust Fund were significantly lower than anticipated.

This basic tax incidence finding has been shown several times. For a recent example, see, Dongwoo Kim et al, “The incidence of Social Security taxes on teacher wages and employment”, Journal of Pension Economics and Finance (2025), 24, 351–370.

This estimate defines “compensation” as wages and salaries plus the employer share of payroll taxes and counts that employer share as one of the personal taxes paid by Americans. This excludes from “compensation” the value of employer benefits, which add about 14.3% to the wage bill. (Some reform proposals would tax part of these benefits as income.) but since the wage bill is only about one-half of all personal income (this surprises some people), the burden on incomes overall is about 16%.] One can jigger these numbers in a number of ways, but this percentage is consistent with the OECD estimate and therefore useful for comparison purposes.

Bernie Sanders, for example, has proposed that wages above $250,000 should be taxed for Social Security but earnings above this limit ought not to raise benefits.

Here are the SSA descriptions of these proposals. For investment income: “Apply a separate 12.4 percent tax on investment income as defined in the Affordable Care Act (ACA), with unindexed thresholds as in the ACA ($200,000 single filer, $250,000 for married filing joint), starting in 2027. Proceeds go to the OASDI Trust Funds.” For S corps: “For active S-corporation officers and limited partners, apply a 16.2 percent tax on investment income as defined in the ACA, with unindexed thresholds as in the ACA ($200,000 single filer, $250,000 for married filing joint), starting in 2026. Proceeds go to the OASDI Trust Funds for tax attributable to 12.4 percent of the total 16.2 percent tax rate.”

The share of Trust Fund income that comes from this source was only 2.2% of income in 1990, is 4% now, but will be above 6% of income after 2035.

Basically, half of the Social Security benefit is added to something close to AGI and a discounted marginal tax rate is applied based on the resulting combined income. The discount is an upwardly sliding scale that runs from 50% to 85%. %). Benefits that contribute to a combined income above $32,000 (for a married couple) are partially taxable, first at a 50% proration eventually rising (for those with a combined income greater than $44,000) to 85%of benefits. For a married couple with typical Social Security Benefits (I picked $44,000 per year; that’s $1800 per person per month; this adds $22,000 to the “combined income” [why is the tax code so complicated?]), the tax is negligible for filers with AGIs (excluding these benefits) less than $30,000 and maxes out for AGIs above $60,000 (cash income greater than $100,000). At that point, the tax on benefits would be 18.7% (0.85 times the marginal rate of 22%). These percentages were my own back-of-the-envelope calculations based on the relevant IRS form. I don’t think there is a “cliff” in these rates. This is so complicated!