Fun with COLAs

Fixing Social Security, Part 5

Post 62: 12 May 2026

This week, I continue my series on Social Security reform by considering how benefits are updated over time for inflation. The next post will focus on the benefit structure, in particular, the degree to which it can be described as “progressive”. I should then be able to wrap up the series by considering the broader question of how Social Security ought to interact with markets.

Originally, I planned to treat cost-of-living adjustments as a minor topic within the broader question of how benefits ought to be set, but—as you will see—COLAs raise some interesting issues of their own. How we set the COLA has an especially big impact on the resources we provide for our oldest retirees. This led me to re-evaluate what the COLA is supposed to do in the first place, and whether we need to modify the approach overall, or at least for long-time retirees.1

COLA Diets

Right now, social security benefits are adjusted for inflation based on the third quarter year-over-year change in the CPI for urban workers (CPI-W). A simple way to save money in the Trust Fund is to go on a COLA diet. And the simplest of these would just shave something off the current calculation. Reducing increases in benefits by 1 point below inflation—which has been proposed—would cut benefits significantly over the long run. Total costs could be reduced by the equivalent of a 2.75% payroll tax or about half of the Fund shortfall.

The thing about changes in COLAs is that they can feel minor in the short run—indeed, if we made the one-point shift right now, the Fund would still run out of money (perhaps a year or so later)—but the effects really add up. In the long run, this cut is draconian. If it had been in place between 2000 and 2025, a 2000 retiree would be facing a benefits cut of one-third.

Mostly, the debate around COLAs occurs in a more confined policy space.

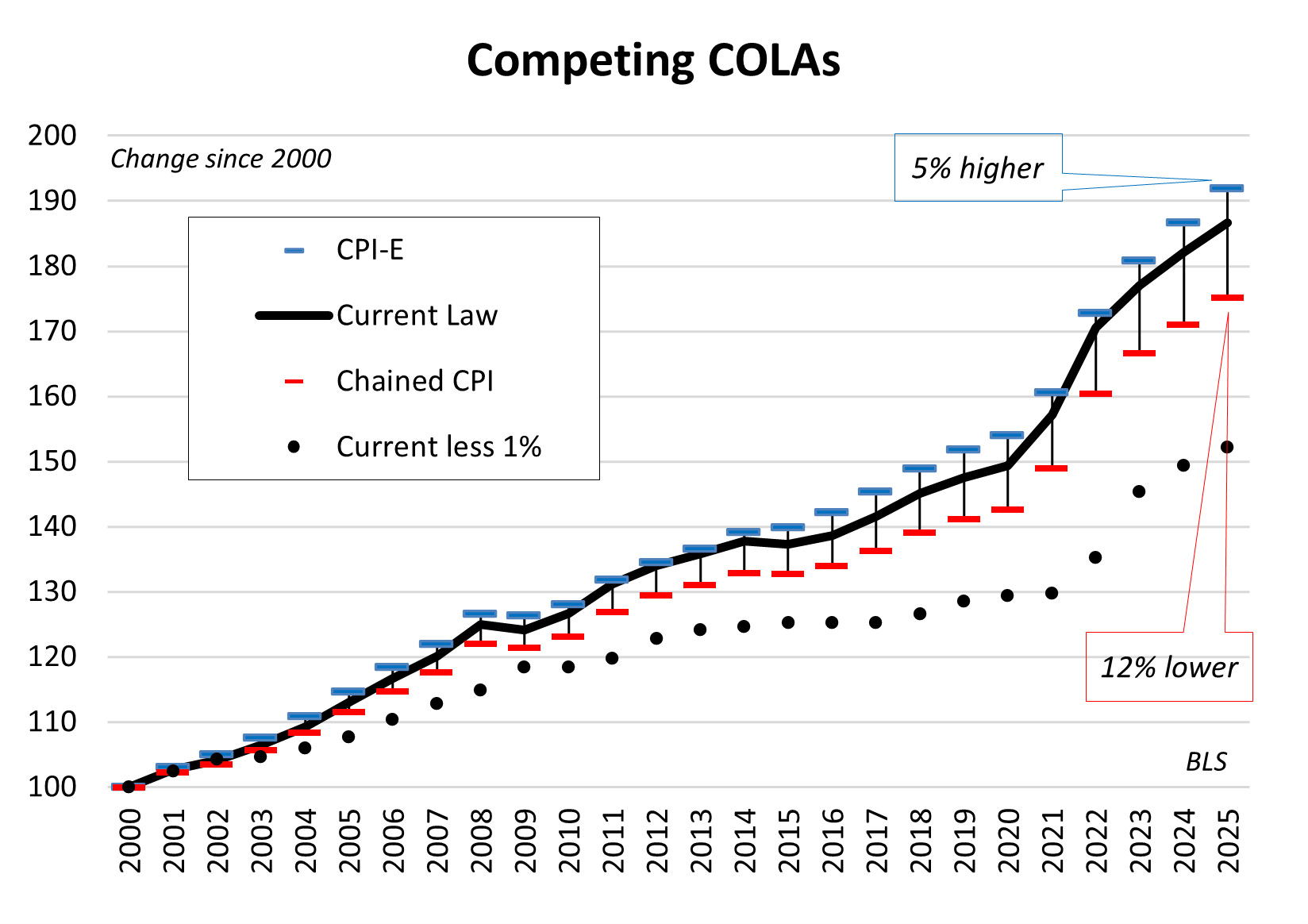

Conservatives tend to advocate shifting from using the CPI-W to the so-called “chained CPI” to calculate the COLA. This construct adjusts the CPI for the fact that consumers make substitutions in their own market basket in response to rising prices. This has the effect of lowering measured inflation as actually experienced by individuals, typically by about three-tenths of a percent per year, on average. If this index had been in place between 2000 and 2025, those retired over this whole period would be receiving about 12% lower benefits now. Not quite the sledgehammer of a 1-point cut, but significant.

The chained-CPI is a theoretical fig leaf designed to mask benefit cuts. I’m not saying it has no basis in theory. People do make these sorts of substitutions, but I am left with two reactions. First, we make a lot of CPI adjustments across different policy arenas and we don’t take this step for any other CPI adjustment. Why would we do so here? If this is better measure of inflation, we should adopt it for all purposes. This connects to my second reaction. The whole point of a cost-of-living adjustment is to capture rising costs of a fixed market basket—the intent is for people to maintain their purchasing power. The fact that they adapt to reduced purchasing power by changing their personal basket of goods is off point. This proposal is the result of a search, not for a more authentic metric, but for a slower-growing index—by definition, the chained CPI must grow slower than the CPI.2

The progressive counterproposal is to use the CPI for elders (CPI-E). This CPI uses a slightly different market basket of goods tailored to seniors. It tends to run about three-tenths of a point per year faster than the CPI-W—though in some years the two are more similar. If we had been using that index since 2000, benefits would be about 5% higher than they are now for people who were retired then.

The chart below shows the path of these CPI-based COLA adjustors since 2000. It plots the CPI-W (current law), the CPI-E, the chained CPI, and the CPI-W trimmed by 1 point. This gives a sense of how big the differences get and how long it takes for them to be significant. Cost-of-living adjustments are time bombs. These changes affect the oldest retirees the most simply because they are subjected to them for longer periods. That segues to my next problem.

Inflation or Quality-of-Life Parity?

Since the proposals to use the chained CPI and the CPI for seniors pull by about the same amount but in opposite directions, a reasonable political resolution to the COLA issue is simply to stand pat. “Compromise” here means doing nothing. But I have a deeper question—or problem—that leads me to wonder whether adjusting for “inflation” is the right approach at all.

That needs an explanation.

The fundamental question here is how Social Security benefits should be adjusted over time in order to treat every cohort as fairly and in as comparable a manner as possible. This is what the first principles of social citizenship require. Since we change the rules of the system from time to time, some intergenerational inequities are inevitable, but we would like to minimize these issues. The problem is that it is not immediately clear how to do that.

The Social Security system uses two mechanisms for aligning benefits over time. The two reflect different aims that ultimately conflict. At retirement, initial benefits are set based on lifetime earnings using a method that is indexed to the average national wage. This procedure solves the problem of how to “add up” earnings that occurred at very different wage-price levels by comparing each individual’s earnings to the national average wage each year. This normalization is based on the standard of living. It works fine. The method ensures that the initial benefits received by each new retiring cohort rise based on the general progress of the economy. My initial benefits reflect where the society has been over the course of my career (and my relative place within it). Because of the normal life cycle of individual earnings, this snapshot is weighed heavily toward the latter part of that career, when earnings are a bit higher relative to that national average. [I’ll go more deeply into how initial benefits are set in my next essay.]

After the initial benefit (the “primary insurance amount” or PIA) is set, benefits increase from year to year based on inflation. That is, we adjust benefits to maintain their purchasing power. This is related to, but very distinct from, the standard of living inputs used to set the PIA. Even if we got the inflation adjustment correct—and it is hard to get it correct—the best we can do is to “lock in” the living standard crystalized in the initial benefit determination.

We hope and expect the standard of living to rise over time, but the inflation adjustment will not account for that. Since (we hope that) real wages will rise over time, subsequent cohorts of retirees will begin their benefits at a higher basis than earlier cohorts. At any given moment in time, this means that older retirees get lower benefits than younger ones.

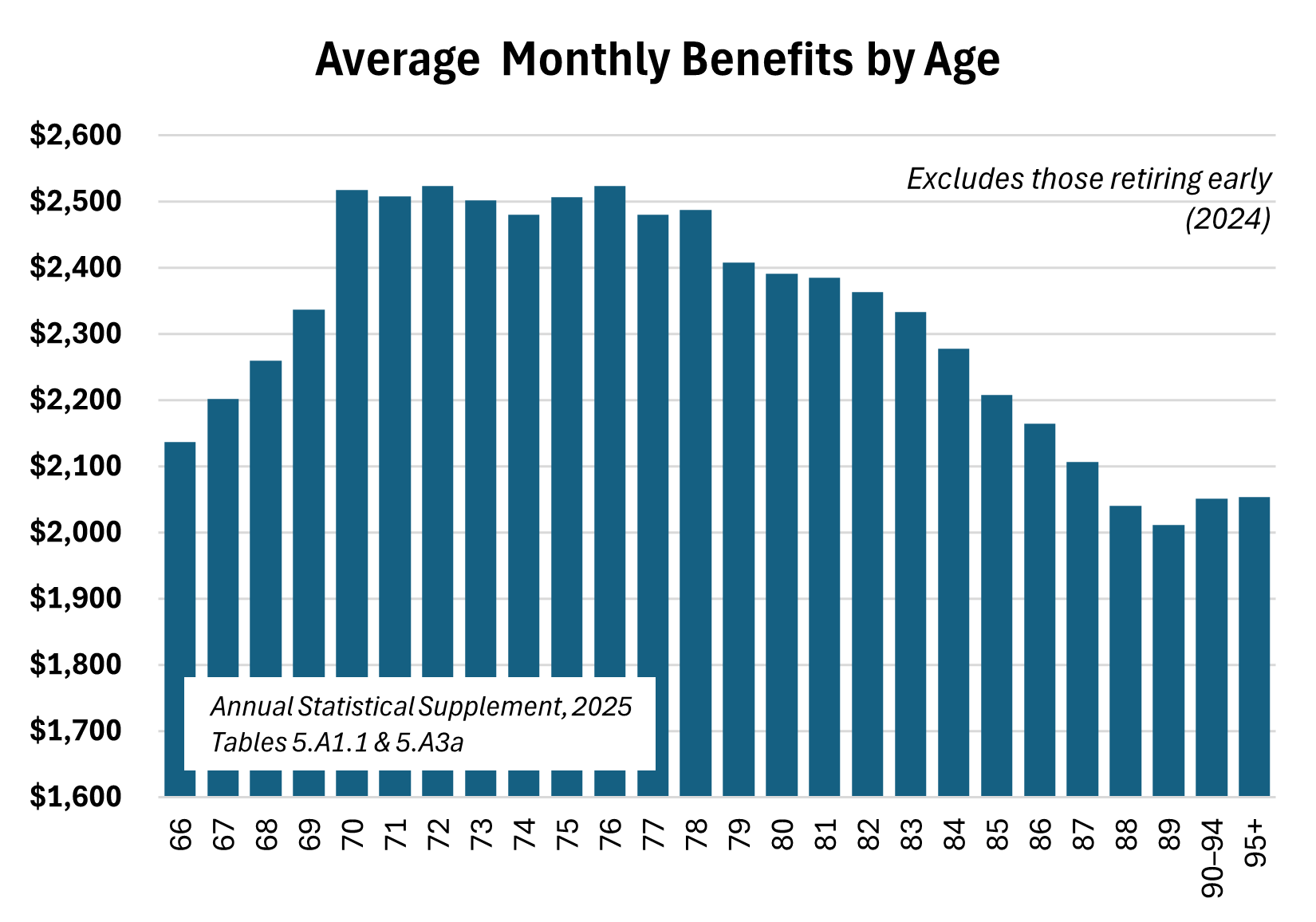

This is evident in the data. The chart below shows the average monthly benefits received by retirees in 2024. The data exclude those retiring early with reduced benefits (but not those retiring later with those incentives added, which is why this peaks at 70). Retirees now in their late 80s receive about $500 per month less than those who retired within the past ten years.3 Use of the CPI-E deflator would not have changed these results much. My own back-of-the-envelope calculation suggests that, had this COLA method been in place for all these retirees, the monthly gap would have narrowed, but only by less than $100.4

The shape of this curve troubles me. We need to evaluate this empirical fact through the lens of social citizenship. Those principles require that everyone has access to the resources they need to fully participate in society. It could well be that the lower cash benefits are not problematic in these terms. Older people may need less income even as they require more non-cash support, especially with medical care and support for daily living. The evaluation must be holistic in this way, beginning with a conception of what “full participation” means for someone twenty years into retirement.

A social citizenship-based evaluation may find that the $3-4 thousand dollar per year difference between does reduce their ability to participate in society fully. We could address this issue by dropping the CPI-based COLA altogether and scaling all social security benefits over time using the same national average wage concept that feeds into the initial benefit calculation. This would raise benefits substantially for all cohorts—I estimate by about $300 per month on average— but, compared to current law, more so for those who are retired for longer. This may be the “correct” answer because its aim would be to preserve living standards relative to a rising national living standard rises rather than purchasing power relative to rising prices. Changing to this model now, however, would be very expensive and help many who are already well resourced. We should only do it if we believe that the general benefit level ought to be higher for everyone (a strong possibility).5

Another approach is to short-circuit the regular cost-of-living adjustment and simply raise benefits for older retirees. Several proposals like this have been made, usually targeting seniors aged 85 or older, or those 20 years into retirement. Early proposals along this line suggested a 5% benefit increase for these older retirees, more recent proposals are more complex but aim in the same direction. In her larger package of reforms, Rep. Gwen Moore (D-WI) has proposed stepping into this benefit increase over five years. This change would significantly flatten the above graph. It would also not be especially expensive, since only about 10% of retiree beneficiaries are this old. It equilibrates at the equivalent of about 0.3% of payroll, making the Trust Fund deficit about 7% worse. This is affordable within the framework I set out in a recent essay, but only if we evaluate this issue as an area of need.

That’s all for today.

This series keeps expanding. Here’s an overview:

Part 1: What is Social Security For? [Post 58]

Part 2: America Aging in Place [Post 59]

Part 3: Paying for Retirement [Post 60]

Part 4: When Should We Retire? [Post 61]

Part 5: Fun with COLAs [Post 62]

Part 6: Making Social Security Progressive

Part 7: Social Security and Market Risk

My goal, as always, is to ground the analysis of social policy in the principles of social citizenship that insist that everyone has a comparable ability to participate in society as full and equal members and, consequently, must have access to the resources that this participation requires as a matter of right. These broad principles are reasonably easy to declaim—I do so regularly—but actual policies get messy fast. This exploration of Social Security details makes that pretty clear, but it also demonstrates the value of keeping the deeper principles in view at all times.

<All of the posts in On Social Citizenship connect. I recommend that readers go back and read the first entry in the series.>

Notes (verbose notes today)

Besides simply accepting the estimated 22% cut in benefits that will come when the Trust fund is exhausted, there are two basic benefit-cutting strategies available to lawmakers: tweaking the formula that sets everyone’s initial benefit or primary insurance amount (PIA), my next topic, and changing how benefits are adjusted over time for inflation. For the moment, I’ll assume that the Fund will be “saved” somehow, mostly because I can’t imagine running for reelection as a Member of Congress the year after it fails, but there is a scenario in which the village is saved only by burning it down. I’ll get to that in the last essay of this series.

The chained CPI always grows more slowly because these substitutions are driven by the desire to lower costs. Total costs could rise faster than the inflation of the CPI’s fixed basket of goods because of other changes in the actual basket of goods people buy, but that is irrelevant to the CPI metric (as, I argue, any shifts in the basket to save money are irrelevant). For other purposes, the fiction of a fixed basket of goods is not relevant. For example, for GDP calculations, the set of goods and services purchased is just that.

Some economists are definitely in on this ruse, but most are just naive practitioners of their dark arts. They sincerely want to measure inflation better (as we do for the GDP) and have lost sight of why we are doing so. A solid argument may be made for revising the “CPI” to a chained version for all purposes (i.e., make this what “inflation” is). Until we do that (we won’t), leave the retirees alone. Truthfully, if we did make that change, it would lend support to my view that a broader standard-of-living metric (based on real wages) is more sound. For now, our aim is to preserve purchasing power, which requires a fixed market basket of goods.

That said, the BLS is always struggling with the technical problem of how to update the market basket over time as products and services come and go (so the market basket is never really “fixed”). That is a topic for another time if it is not entirely beyond me (it gets weedy fast). But the effect of “measurement” on “policy” is a general problem in public policy—this is just one instance of it—that is worth exploration. My basic point here is that, in this case, arguments about measurement are being used to mask policy positions and make them seem more reasonable. The causation must go the other way.

I constructed these data by combining two tables in the Annual Statistical Supplement, one showing all retirees and one showing early retirees. It would be nice to compare benefits for only those who retired at the full retirement age; I’ll keep looking for data. The fact that wealthier Americans—who receive higher initial benefits on average—live longer and are therefore over-represented among these older retirees (something I reported on in the last essay) means that the “real” effect here is greater than these averages suggest. To control for that, I’d have to compare the life path of those who had “typical” benefits when they retired at full retirement age. This seems like a lot of work, but it may be worth doing.

To estimate this, I assigned a year of full retirement to each of these cohorts and back-estimated an initial average benefit for each using the CPI-W, then reinflated that using the CPI-E. This is a very rough way of doing this, but is broadly correct and should yield conservative estimates. A similar exercise using the “national wage index” (the average wage that Social Security uses in the original benefit calculation, raises everyone’s benefits but has the most impact on those retired for longest. Overall, it generates a flatter curve.

Note that these historical backcasts depend on the actual path of wage and price growth since the mid-1990s (for the current population of retirees). Academics would say that the results are contingent. For much of the backcast period, inflation was very low and real wage growth sluggish. The future could look very different.

The shift from one COLA system to another could also be made in steps that limit the amount of benefit increases in any given year, probably relative to inflation. This would be done for Trust Fund management purposes (only) with an eye towards smoothing out the impact of the change over, say, a decade.